Introducing First Pillar

Happy summer! Not only does July mark the one-year anniversary of Radix Financial Cayman, but we’re also thrilled to announce the formal launch of our first private fund ̶ Radix Financial First Pillar Ltd. Through First Pillar we expand access to both our flagship Global Growth and Income Reserve investment strategies at much lower minimums than were previously possible through separately managed account portfolios. And while not (yet) open to our US investors, First Pillar marks the realization of a multi-year ambition to create a solution that provides clients our professional expertise while simultaneously eliminating many of the unnecessary roadblocks, fees, taxes, and complexities experienced by non-US investors.

We invite you to further explore the opportunity via the link below:

Stocks are Back!

Major stock market indices made significant gains in the first half of the year due to improving inflation, slowing Fed rate hikes, the absence of a recession, a more stable banking sector, and a strong rally in tech stocks. The S&P 500 has climbed 16.9% on a total return basis, while the Nasdaq and Dow have returned 32.3% and 4.9%, respectively. Markets have recovered much of their losses from last year with the S&P 500 now 7% from its all-time high. The rest of the world has also returned a respectable 9.47% YTD as measured by the MSCI All-Country World Index Ex-US. But even after this exceptionally strong year-to-date performance, many investors remain skeptical whether this is truly the beginning of a new bull market or simply a "dead cat bounce” along a continuing downtrend.

There will always be reasons to see the glass as half empty, especially with many uncertainties still looming. Challenges continue in the wake of the bank failures earlier this year, most notably in highly leveraged sectors like real estate. Upcoming refinancing activity could test the stability of the system as rates remain high and lending activity tightens. Additionally, while a debt ceiling crisis was averted, the can has only been kicked down the road to the beginning of 2025. In the meantime, geopolitics continue to be problematic as U.S. relations with China and Russia remain strained. Next year’s US presidential election will also soon be at the forefront as markets assess all of these risks.

However, experienced investors (like all of us) with a broad perspective on markets, know that there are always risks that must be balanced against long-term returns. These risks often feel insurmountable as they are occurring but, once they are in the rear view mirror, investor concerns shift to whether the recoveries are sustainable. Since the publishing of our (at the time) hotly controversial October commentary, the S&P 500 has notched three consecutive quarters of strong returns, a full 180-degree shift from the bear market returns experienced during the first three quarters of last year.

Great. Does that mean the recession is cancelled?

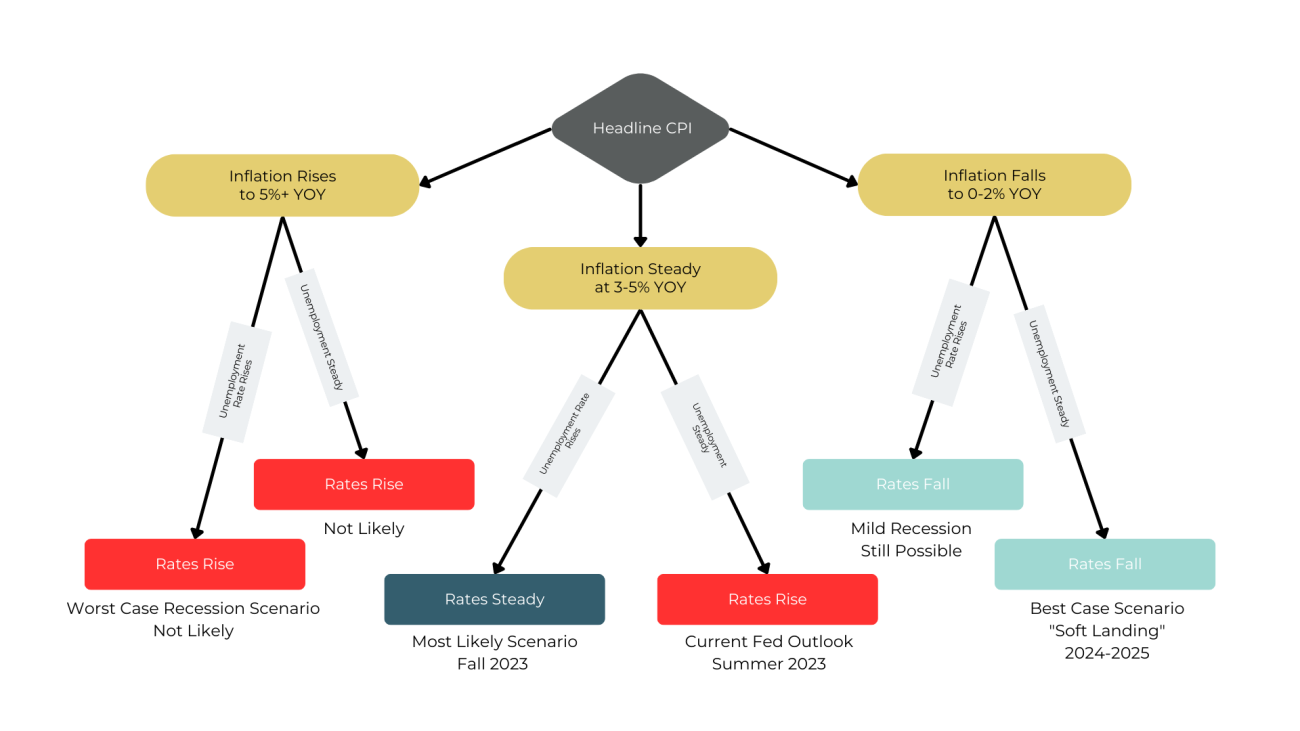

Only a year ago, the prospect of the Fed achieving a "soft landing," i.e. that inflation would improve without a recession, seemed far-fetched, even to optimists like us. The headline Consumer Price Index (CPI) has decelerated from a peak of 9.1% a year ago to 3% today, the lowest since March 2021. However, core inflation (excluding food and energy) remains sticky at 4.8%, and the Fed has made it clear they are committed to returning inflation to their 2% target by keeping rates "higher for longer." Inflation is cooling, so while the threat of multiple further rate hikes this year is real and should not be ignored, we consider much to be rhetoric as they wait and see if the data continues to move in the right direction.

The FOMC’s strict “data driven” playbook allows us to invest around what direction interest rate policy will likely take by extrapolating trends in CPI and non-farm payrolls data. Based on these relationships, the flow chart below reflects the possible paths we believe rate policy could take over the rest of 2023. Simply put, so long as CPI remains elevated above the Fed’s 2% target, we expect rates to continue to push higher, but only until their actions result in consequences to the US labor market.

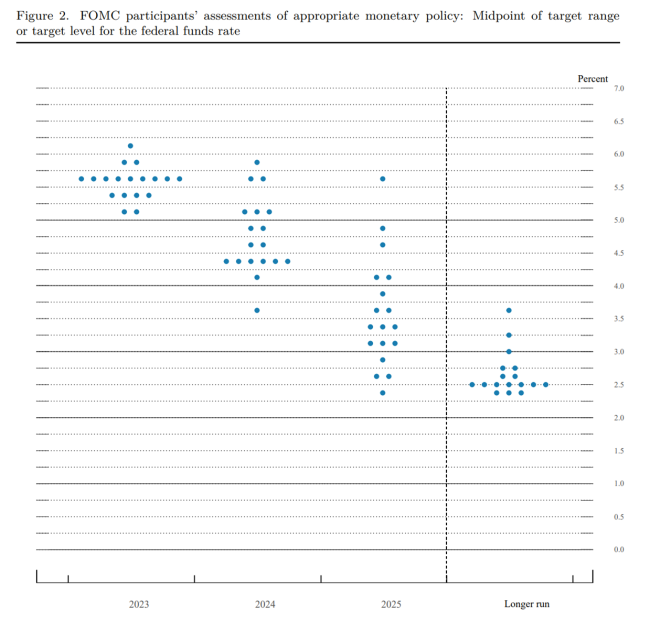

If you need further reassurance, FOMC participants regularly update us where they think rates will be over the next three years, as published in the dot plot below. As of June, all members believe that rates will be stable or higher through 2023 before slowly coming down over 2024-2025 to settle at a comfortable 2.5ish percent for the longer-term.

The persistent inverted shape to the US Treasury yield curve, however, signals that the market still doesn’t believe them. Market action points to the belief that short-term rates will fall sooner rather than later and in response to recessionary and/or political pressures. Believe what you will, but our most likely scenario is that the Fed adopts an extended pause around 5.5% for the rest of 2023, and will slowly begin to ease rates to combat rising unemployment starting in 2024.

Conclusion

Markets rebounded in the first half of the year, catching many investors off guard. While markets never move up in a straight line, investors who focus on long run fundamentals and avoid trying to time the markets will likely be in a better position to take advantage of market opportunities in the second half of the year.

Portfolio Changes

During Q2 we adjusted equity exposures to bring down positioning in emerging markets. Emerging market equities continue to lag behind developed markets and we believe they will continue to face substantial headwinds in "higher for longer" rate environments.

In addition, continued market recalibration and discrepancy amongst styles and sectors allowed us to pick up several opportunities in the Core Equity portfolio during the quarter:

Amazon (AMZN) was sold from the portfolio to make space for new positions, after a 4 ½ year holding period and over 80% cumulative return. We expect Amazon.com will continue to dominate as an online marketplace, however margins have been severely crimped over the last year. And while we see AWS as a leader in the continued transition to cloud computing, we hold several other companies in the cloud space whose earnings are not being used to supplement weakness in ecommerce.

In a play for exposure to discretionary spending, we added a position in Novo Nordisk (NVO), the first-to-market pharmaceutical company focused on the weight loss market with its blockbuster anti-obesity drugs, Wegovy and Ozempic, which were originally intended as diabetes treatment. Despite competition from other players in the diabetes market, FDA approvals can take years. Even then, analysts estimate the market for anti-obesity drugs, currently $2.4 billion, could touch $50 billion by 2030, leaving plenty of room for multiple players to profit. We believe this is a potential game changer in the personal health care market, as the percentage of Americans considered obese has nearly tripled over the last 50 years.

We exited our position in Ciena Corp (CIEN) due to continued slow execution resulting from supply chain issues. We worry that clients will grow impatient and find alternative solutions, or simply not be in the same financial condition through this phase of the economic cycle to be able to follow through on these network infrastructure build outs or upgrades.

Airbnb Inc (ABNB) was added to the portfolio as a way to play the continual pent-up demand for travel following the pandemic lock-down years. The online rental platform for short-term home rentals offers attractive profit margins (+23% net) and has become the go-to platform for those looking for rental homes. “Airbnb” has strong brand recognition and has become a general term for home rentals - much like Google has for internet search (I’ll just “google” it to find out). Given the company focuses solely as the online platform, connecting renters to hosts, and does not own the underlying real estate, we see advantages over traditional hotel stocks to tap into the travel market.

Within the healthcare sector, we rotated out of Johnson & Johnson (JNJ) and used proceeds to purchase Pfizer (PFE), which has sold off as demand for the Covid-19 vaccine has declined. We believe this to be an attractive entry point for Pfizer, a company with strong profit margins and high free cash flow for acquisitions. JNJ was held in the portfolio for over eight years and offered an average annualized return of +6.7% over that holding period. The company is working towards completing the spin-off of its consumer health segment in 2023 and continues to face headwinds from the baby powder talc litigation. We see better opportunities for capital appreciation in Pfizer at current levels, so we decided to make the swap.

Also in the healthcare sector, we sold Illumina (ILMN), the genetic sequencing company. While we continue to have high hopes for the incredible early cancer detecting technology Illumina is providing to genomic research centers, laboratories and hospitals, we are not comfortable with the level of risk associated with the near-term outlook. Regulatory scrutiny over the Grail acquisition moving out of Illumina’s favor, a proxy fight with activist investor Carl Icahn and the departure of CEO, Francis deSouza, all lead to an uncertain near-term future for the company. In its place, we purchased shares of Intuitive Surgical (ISRG), a medical device company that manufactures the Da Vinci robotic surgical systems. The company saw a strong recovery this year in its elective procedural volume and guided forward growth rates higher for the remainder of the year.