Tax Cuts & Jobs Act of 2017: What It Means For Us

Happy New Year! What a year 2017 turned out to be. The S&P 500 returned over 20%, finishing all 12 months positive, something that has never happened in the history of the US equity markets.

In December, Washington passed the Tax Cuts and Jobs Act of 2017. While most of the legislation deals with corporate tax reform, there are many Easter eggs for household level finances as well.

1) Tax brackets, standard deduction, and child tax credit

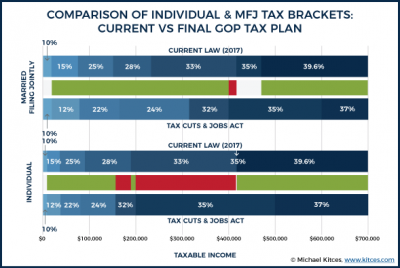

Most Americans will see a reduction in their tax bill for 2018. Seven regressive tax brackets remain. Those married filing jointly, who earn between $240k and $315k a year, will see their tax bracket slide from 33% to 24% — a huge 9% reduction. A chart from our friends at kitces.com illustrates the changes:

Most of the itemized deductions were retained within the Jobs Act, except some great things like tax preparation and investment advisory fees. The standard deduction is being doubled, and the refundable child tax credit has been expanded.

2) Estate and gift tax

One of the more controversial provisions is effectively a doubling of the estate tax exemption. Individuals can now pass $11.2 million (double for married couples) down to their heirs both estate and capital gain tax-free. However, this provision will expire in 2025.

There is a huge step-up in basis at the date of someone's death — heirs receive assets tax-free at market value. Individuals can also give $15,000 to as many other individuals as they wish each year without tax. I call this the "Oprah Rule."

3) Qualified dividend and long-term capital gains

Income from qualified dividends and long-term capital gains will continue to qualify for preferential tax treatment. The qualified dividend and capital gains tables seem to have been forgotten within the new act and will instead be based on what tax bracket you would have fallen into under pre-2018 law.

4) 529 Plans

Under the Jobs Act, funds within a 529 Plan can now be utilized to pay for private secondary education or homeschool expenses up to $10,000 per student each year. When you start removing funds earlier, it diminishes the opportunity for tax-free growth.

Example: A family contributing $250 a month for 18 years at 5% returns ends up with $87,300. A one-time gift of $54,000 at birth at 5% yields $129,957. That's tax-free growth of nearly $76,000!

Before even thinking about a 529 plan, always make sure you're maxing out your Roth options (IRA and/or 401k).

Sincerely,

Amy Hubble, CFA, CFP®