The Stock Market Doesn't Care About Your Feelings

Happy Summer!

Some days, it feels like the whole world has gone crazy. If you'll indulge us for a moment of candor, these are some things we’ve been hearing in conversations lately, and frankly, feeling ourselves. Nothing to do with official economic data or valuation models—just the kind of thoughts that seem to be sitting in the background for a lot of people right now. Maybe you feel the same?

- Everything feels expensive. Food, travel, software subscriptions, insurance, healthcare—prices have drifted into an alternate reality.

- We’re overdue for a market correction. We’ve enjoyed four years of double-digit returns, and the party can’t go on forever, right?

- The political environment is exhausting. Market-moving rhetoric over tariffs, taxes, wars, and executive actions change the investment landscape daily.

- Nothing is easy. Are we imagining it, or has even the simplest administrative task—like renewing a license, getting a real person on the phone, or resolving a billing issue-become an impossible undertaking?

- Retirement and taxes are overcomplicated. The rules have become a tangled mess; even experienced advisors are struggling to keep up.

- Will we ever really reach a lasting “cease-fire" with Iran? And what was the point?

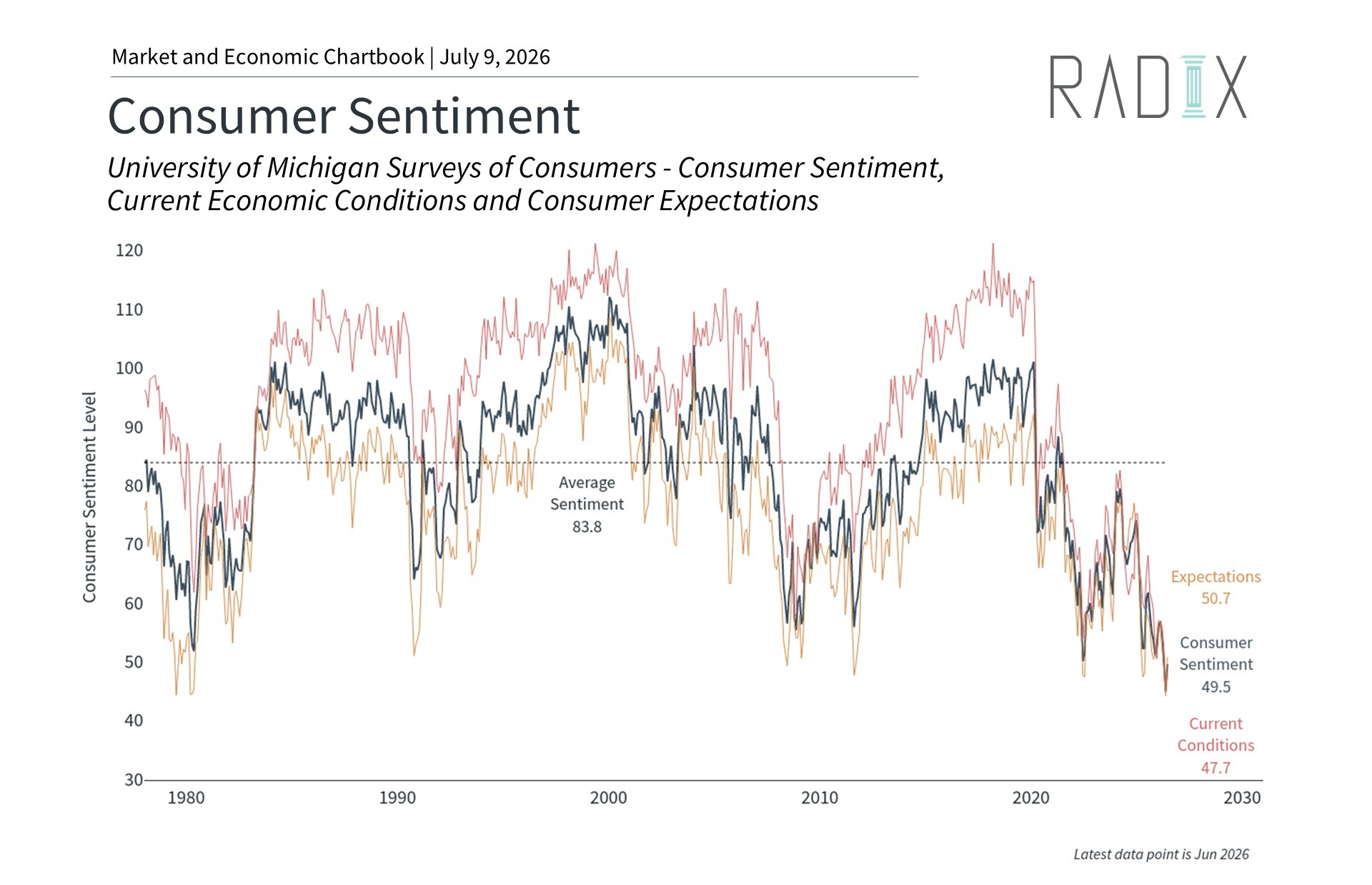

And we know we’re not alone. Take a look at the most recent consumer sentiment numbers from June in the exhibit below. The University of Michigan run survey measures how consumers view prospect for their own financial situation, how they view prospect for the general economy over the near term, and their view of prospects for the economy over the long term. As you can see, the readings are DISMAL.

Then there's the stock market.

Despite all of those worries, the market has continued climbing to new highs. These conflicting signals reflect an economy that is performing well overall, but is also leaving some households feeling stretched.

For long-term investors, understanding both sides of this picture is important.

Are the Markets Ignoring Reality?

The answer begins with recognizing that the stock market and our day-to-day experience of the economy are not the same thing.

The economy is what we live every day. It's the grocery bill that catches us off guard, the insurance renewal that costs more than expected, the frustrating customer service experience, or the headlines that leave us questioning what comes next.

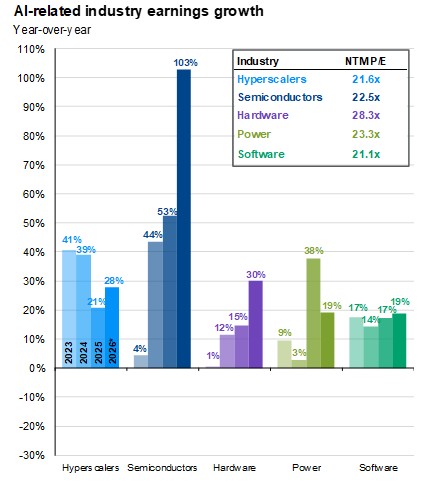

The stock market, by contrast, is constantly trying to estimate what businesses will earn six months, a year, or even several years from now. Investors aren't buying today's economy; they're buying tomorrow's earnings. Particularly, they’re buying the earnings growth of an increasingly high concentration of companies spearheading AI infrastructure, as you can see in the chart below:

That's why markets can rise even when today's news feels discouraging. They aren't ignoring today's challenges, they’re just asking a different question: Will businesses be more profitable in the future?

What Could Change the Market’s Mind?

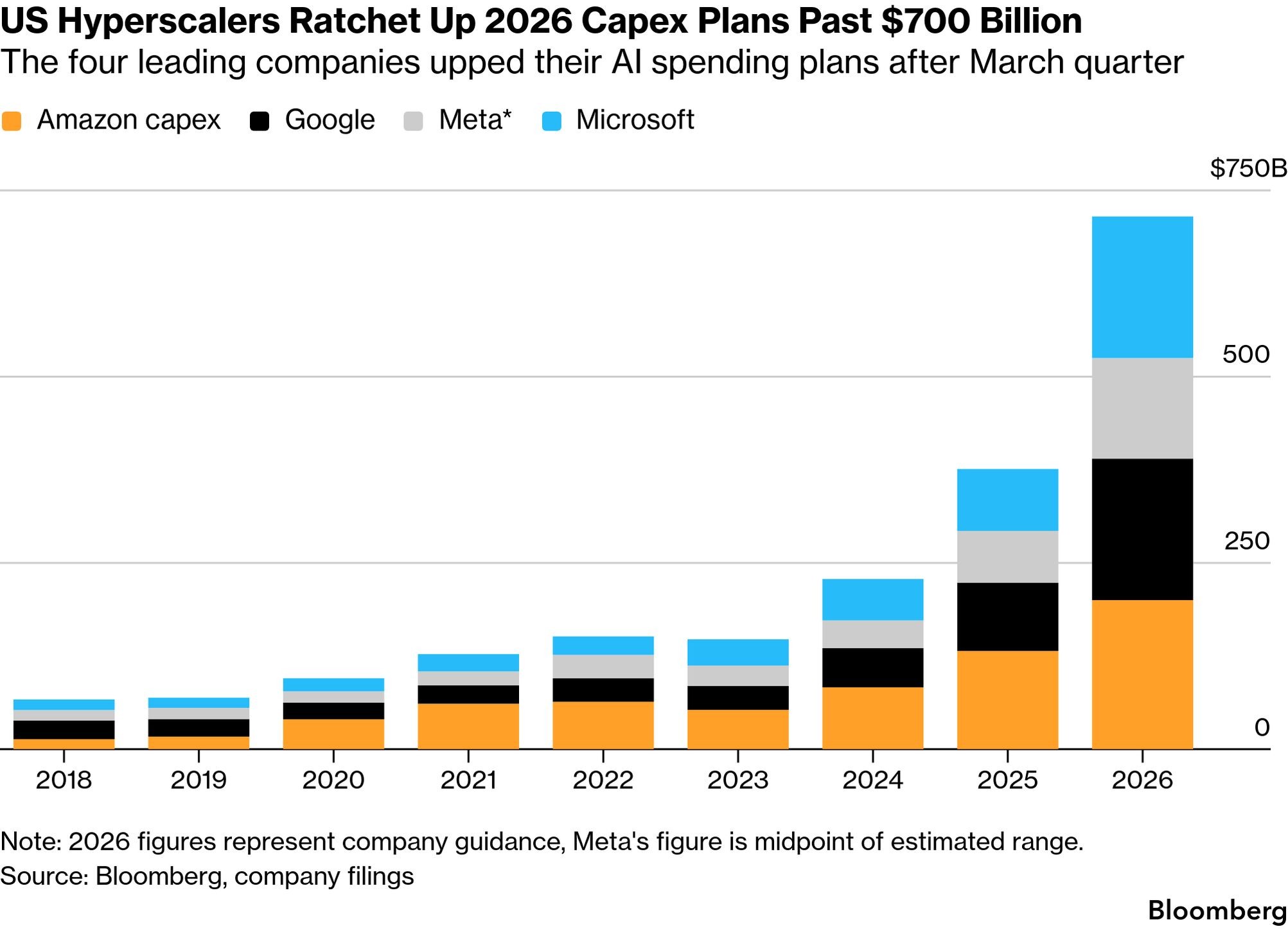

In our view, the biggest risk is still inflation, specifically supply-side inflation. When key inputs become scarce, businesses are paying more to produce the same goods and services. It squeezes margins, delays investment, and makes it harder for companies to deliver the future earnings investors are expecting from the eyewatering dollars of capex the hyperscalers are currently pouring into AI infrastructure.

So far, the market has rewarded companies spending these extraordinary amounts of money because investors believe that spending will eventually translate into higher profits. That’s the trade-off. Companies spend now, earnings arrive later. But this relationship can breakdown when the inputs required to build AI infrastructure become scarce and expensive.

Memory is one of the clearest examples we’re seeing today. Micron recently reported record fiscal third-quarter revenue of +346% YoY with operating margins of 80%. Similarly, SK Hynix, the South Korean global leader in high bandwidth memory, reported revenue growth of+198% YoY with the average selling price for DRAM AI chips (don’t ask) rising over 60% in just the first quarter. Both reported backlogs of over three years of capacity to produce.

That is great news for the companies producing scarce memory. It’s less great for the companies that need to buy it. Increasing chip supply isn’t easy, so the shortage is effectively causing a bidding war. Microsoft announced another Xbox price increase, specifically citing storage and memory prices that had increased by more than 2.5x, while Apple reportedly raised prices on parts of its Mac and iPad lineup as rising memory and storage costs became harder to absorb.

That’s the part we’re watching. If memory costs keep rising, then the companies making the largest AI investments need to produce even larger future earnings to justify today’s spending. For markets, the concern is that inflation could raise the cost of the AI capital expenditure boom at the exact moment investors are demanding clearer evidence of future returns.

There are political implications too. The Trump Administration desperately wants the U.S. to maintain leadership in the AI race, while also limiting China’s access. Those goals don’t fit neatly together. Encouraging domestic capacity may be politically attractive, but it takes years and enormous capital to build out. Allowing cheaper components into the supply chain from China would relieve pressure and allow American companies to keep prices manageable, but it may conflict with national security priorities.

And finally, there is the Fed (did you think we’d fail to mention?!) With the most recent CPI number rising to 4.2% YoY in May, markets are starting to price in the possibility of a rate hike this year. For the avoidance of doubt, we believe this would be a mistake. We don’t believe supply-side inflation constraints can be fixed with rate cuts, and Fed action to the upside risks stagflation and higher unemployment. We certainly don’t envy new Fed Chairman Kevin Warsh as he attempts to successfully maneuver between competing mandates.

What’s the Take Away?

A realistic view of today’s market doesn’t mean we should become pessimists. Investors are already accounting for an unsettled world. What they are rewarding is the belief that companies spending aggressively on AI can eventually convert that investment into profits, and so far, the evidence has supported that view.

Expensive buildouts have happened before. Railroads, electricity, the internet, cloud computing, and smartphones all required enormous upfront investment before their full economic value became clear. There were excesses, failures, and painful corrections along the way, but the long-term result was a more productive economy.

That is why we invest. Not because the world feels calm. It doesn’t. Not because every risk has disappeared. It hasn’t. We invest because long-term wealth is built by owning productive businesses through imperfect environments. And if AI ultimately helps companies become more productive, more efficient, and more profitable, then markets will continue to move higher —even in a world that feels expensive, uncertain, and politically complicated.