One Big Beautiful Quarter

If you had told me the week of April 2nd when the S&P was down 18%, that we would have the opportunity for our flagship strategy to finish the quarter up nearly 10%, notching one of the best quarters in the firm’s 10+ year history…

I would have told you that “Markets have a way of rebounding when investors least expect it. Patience, not panic, tends to pay off.”

Actually. That’s exactly what we said in last quarter’s commentary. But I would never have expected the markets to rebound so quickly.

Investing is sometimes fun like that.

Let’s start with the One Big Beautiful Bill…what’s in it?

After months of negotiations, the “OBBB” was approved by Congress and signed into law by President Trump on July 4. This new budget is far-reaching, including making many parts of the 2017 Tax Cuts and Jobs Act permanent, raising state and local tax exemptions, extending the estate tax limits, and much more.

Unfortunately for our non-US clients, our hope for a full repeal of the estate tax or any increase over the paltry $60,000 exemption on US assets owned by foreign investors was not included. But, for our US-based clients, there is a lot to like.

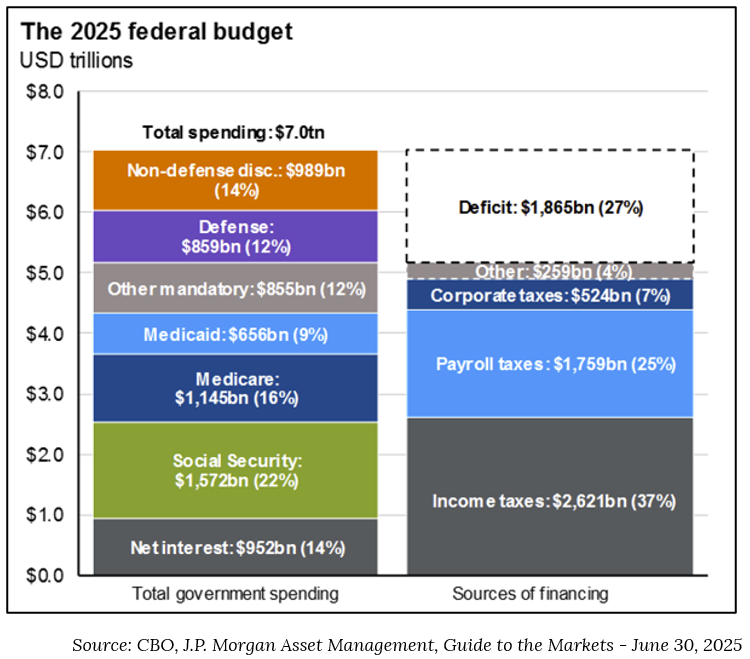

Are you concerned about the deficit?

Government borrowing has increased persistently over the past century and will likely continue to do so. The Congressional Budget Office estimates that this new tax and spending bill will add $3.4 trillion to the national debt over the next decade. This is against the backdrop of a federal debt that already exceeds 120% of GDP, or $36.2 trillion, which amounts to about $106,000 per American.

Pretty ridiculous.

But the US government has something no other country has: control over the global reserve currency. An investment guaranteed by the “full faith and credit of the United States government” has always served as an understood promise that, like the Lannisters, the US always pays their debts.

This surety has served to facilitate perpetual demand for US Treasuries, and for the past century, allowed politicians to spend from the magic money tree that grows in Washington’s backyard.

Several valid concerns have been raised by investors and voters alike whether this is sustainable. On one hand, tax cuts can stimulate economic growth, which may offset revenue losses through increased economic activity. On the other hand, Washington has a poor track record of balancing budgets.

Thankfully, the depth and liquidity of US financial markets, the relative stability of American banking institutions, the parabolic adoption of stable coins, and the dollar’s continued use in international trade and investment give us confidence that (at least for now) the dollar has no viable competitors. But it’s always a risk.

Where are we with the tariffs?

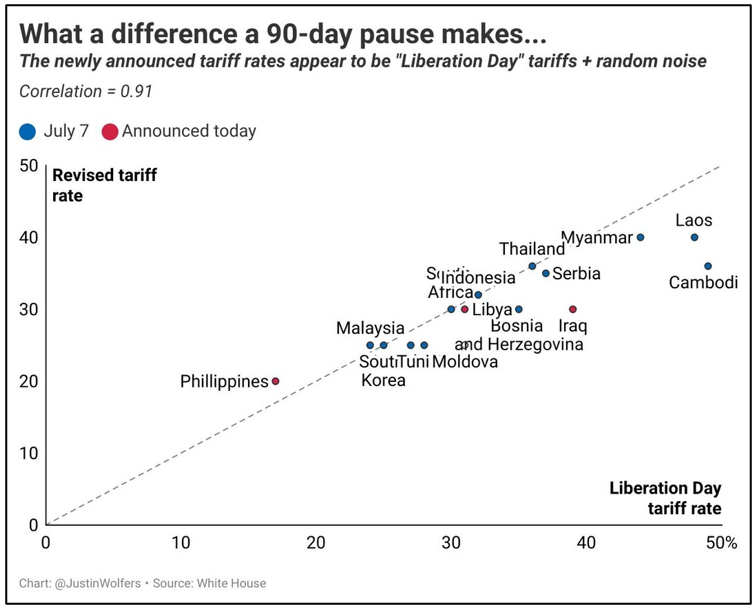

The Trump Administration’s 90-day pause on reciprocal tariffs is up. And (shocker) 90 days was not enough time to get 90 deals done. Despite market protests, the diplomatic geniuses in the White House are refusing to let us off the hook just yet.

This week, the White house “sent”/posted on social media, several “Dear John style” letters addressed to 20 countries, including top ten trading partners Japan and South Korea, notifying them of higher tariffs that will begin on August 1st. This new deadline follows a 90-day pause on the April 2nd “reciprocal tariffs.”

The further delay in implementation is good news for markets, but the fundamental problems remain the same. Multinational companies and the Fed can’t make decisions. And given the rates presented in President Trump’s latest letters, nothing has really changed. Just as it was in April…it’s catastrophic for the American consumer, small business, and the global economy as a whole.

Take Japan for instance, the US’s fifth largest trading partner. An ally, both militarily and commercially, and the largest foreign holder of US debt – at $1.1 trillion. The WSJ cited that a Japanese trade representatives had made seven visits to Washington between April and June, primarily to lobby for the Japanese auto sector, a point of national pride which employs 1 in 10 of Japan’s workforce. Despite the obvious efforts being made, the Prime Minister of Japan “received” a social media post notifying them that the tariff on Japanese goods had been increased from the April 2nd level of 24% to 25%.

This is just one example, but it illustrates the complexities of global trade negotiations and the impossibility of reaching a mutually beneficial agreement under the ever-moving goal posts and impregnable terms the Trump administration is attempting to extort upon its (formerly) closest allies. As for market participants-the theatrics, the on-again, off-again extensions, and the made-up numbers are getting old.

And interest rates? What about those?

It’s July and we still haven’t seen any of the promised cuts to the headline fed funds rate this year. Lots of reasons for this, but the primary being that the Fed is concerned about the impact that the Administration’s tariff plan will have on inflation.

The President has been critical of Jerome Powell’s approach, citing that there has been NO INFLATION. Hyperbole aside, he’s not wrong, headline CPI rose just 2.4% yoy in May, but as David Kelly, Chief Global Strategist for JP Morgan put it:

“the inflationary impacts of tariffs have been delayed, not cancelled.”

Lower interest rates coupled with higher inflation could mean negative real yields for investors, which lowers demand for Treasuries. But continued demand for US debt is a must for the fiscal spending party to rage on. So regardless of the Fed’s short-term rate policy, longer-term market rates along the curve would likely still rise/steepen in response to inflationary pressures and continued deficit spending.

To put plainly – If the US government (The President + Congress + The Fed) cannot (or will not) act to keep inflation in check, it won’t matter if the Fed lowers rates. The crucial 10-year Treasury yield – which heavily influences mortgage rates and serves as a benchmark for refinancing US debt – will go up, not down.

In spite of public threats and insults, an independent FOMC is still the last starfighter against inflation and the country’s best chance at accomplishing the President’s aims for growth and prosperity.

I think it was the Rolling Stones who described the Fed’s job best:

You can’t always get what you want;

But if you try sometimes; Well, you just might find;

You get what you need.

Two Truths

Bottom line – the quarter was great. Really great.

As an economist, there’s a lot of risk in the short-term outlook.

As a long-term investor, opportunities continue to present themselves in both expected and unexpected ways.

Both can be true.

Enjoy the summer!

Amy & Jess